Should You Do a Roth Conversion? Here’s How to Think About It

Roth conversions are one of those financial strategies that are great in theory, but in practice, they can get pretty complex.

A Roth conversion makes sense if you're in a lower tax bracket now than you expect in retirement and can pay the tax bill without touching the converted funds. The best opportunities occur during low-income years like early retirement, before Social Security or RMDs begin. Let's dive into the details.

What is a Roth Conversion?

At a basic level, a Roth conversion means moving money from a pre-tax retirement account (like a traditional IRA or 401(k)) into a Roth account, where future withdrawals are tax-free. The catch? You have to pay income taxes on the converted amount now.

When Does a Roth Conversion Make Sense?

Why would anyone choose to pay more taxes now? Because in the right situation, it could save you money later. Roth accounts grow tax-free, and withdrawals in retirement are also tax-free. That can be a major advantage if you’re currently in a lower tax bracket, expect to be in a higher tax bracket down the road, or want to ease the future tax burden on your heirs. Timing is key: if your income is unusually low in a given year—for example, during early retirement before Social Security or required distributions begin—a Roth conversion could let you lock in today’s lower tax rate and avoid higher taxes later.

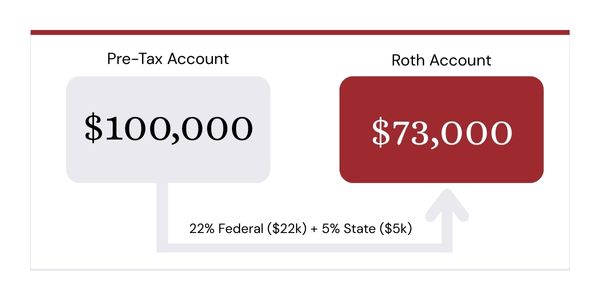

The True Cost of Converting

How much will you owe when you convert? Let's look at an example: if you convert $100,000 from a pre-tax account while in the 22% federal bracket and 5% state bracket, you’ll owe about $27,000 in taxes. If you pay that tax bill from the conversion itself, only $73,000 ends up in your Roth. If you can pay the taxes with other funds, the full $100,000 goes in, maximizing your potential gain from compounding interest. Whether you pay from the conversion or from other accounts, you'll need a strategy for this upfront tax cost.

Even so, if you expect to be in a higher tax bracket in retirement, once Social Security, side income, and Required Minimum Distributions (RMDs) kick in, a conversion now could help minimize future headaches and give you more control over your taxable income later.

There’s also the impact on things like capital gains rates, Medicare premiums (IRMAA), and even the taxability of Social Security. And let’s not forget surprises—like unexpected income or a late bonus—that could bump you into a higher bracket mid-year and wipe out the conversion’s benefits. It's why Roth conversions aren’t “set it and forget it.” They’re most useful when planned carefully and strategically.

Psst...want more information about Medicare planning? Be sure to check out our blog here.

Bottom line? Roth conversions can be a smart move—but only if they fit your broader financial picture. That’s why Frank runs the math across all your real numbers in real time, weighing tax brackets, income sources, and life events to help you decide if and when it makes sense. Because with taxes, timing really is everything.

Frequently Asked Questions

Can I reverse a conversion?

No. Once you convert, it's permanent. This changed in 2018—before then, you could undo conversions, but that's no longer allowed.

What is the 5-year rule for Roth conversions?

Each conversion starts its own 5-year countdown. If you're under 59½ and withdraw converted money before five years pass, you'll pay a 10% penalty. Once you hit 59½, the 5-year rule doesn't apply anymore. You can access your converted money anytime.

Do Roth conversions affect Social Security taxes?

Yes. Conversions count as income, which can increase how much of your Social Security benefits become taxable—potentially up to 85%. It's one of those hidden costs you'll need to plan for.

Frank is an AI-powered service provided by SmartPath Advisors, LLC, an investment adviser registered with the U.S. SEC. Registration does not imply a certain level of skill or training. This content is shown for educational purposes only.